Optimizing Tuning Parameters for Balance

Source:vignettes/optimizing-balance.Rmd

optimizing-balance.RmdPart of using balancing methods, including matching, weighting, and subclassification, involves specifying a conditioning method, assessing balance after applying that method, and repeating until satisfactory balance is achieved. For example, in propensity score score subclassification, one needs to decide on the number of subclasses to use, and one way to do so is to try a number of of subclasses, assess balance after subclassification, try another number of subclasses, assess balance, and so on. As another example, in estimating the propensity score model itself, one might decided which covariates to include in the model (after deciding on a fixed set of covariates to balance), which covariates should have squares or interactions, and which link function (e.g., probit, logit) to use. Or choosing the number of matches each unit should receive in k:1 matching, or which value of the propensity score should be used to trim samples, etc.

Essentially, these problems all involve selecting a specification by varying a number of parameters, which are sometimes called “tuning parameters”, in order to optimize balance. Many popular methods adjust tuning parameters to optimize balance as inherent parts of the method, like genetic matching (Diamond and Sekhon 2013), which tunes variance importance in the distance matrix, or generalized boosted modeling (McCaffrey et al. 2004), which tunes the number of trees in the prediction model for propensity scores. This strategy tends to yield methods that perform better than methods that don’t tune at all or tune to optimize a criterion other than balance (e.g., prediction accuracy) Pirracchio and Carone (2018).

As of version 4.5.0, cobalt provides the functions

bal.compute() and bal.init() to aid in

selecting these tuning parameters in an efficient way without needing to

manually program the computation of the balance statistic used as the

criterion to optimize. This vignette explains how to use these

functions, describes the balance statistics that are available, and

provides examples of using these functions to implement new and existing

balancing methods yourself. These functions are primarily for use inside

other packages but may be useful to users experimenting with new

methods. For a complete way to assess balance for a single

specification, users should use bal.tab() and

bal.plot() instead.

bal.compute() and bal.init()

Broadly, these functions work by taking in the treatment, covariates

for which balance is to be computed, and a set of balancing weights and

return a scalar balance statistic that summarizes balance for the

sample. bal.compute() does the work of computing the

balance statistic, and bal.init() processes the inputs so

they don’t need to be processed every time bal.compute() is

called with a new set of weights.

For bal.init(), we need to supply the covariates, the

treatment, the name of the balance statistic we wish to compute,

sampling weights (if any), and any other inputs required, which depend

on the specific balance statistic requested. bal.init()

returns a bal.init object, which is then passed to

bal.compute() along with a set of balancing weights (which

may result from weighting, matching, or subclassification).

Below, we provide an example using the lalonde dataset.

Our balance statistic will be the largest absolute standardized mean

difference among the included covariates, which is specified as

"smd.max". We will first supply the required inputs to

bal.init() and pass its output to

bal.compute() to compute the balance statistic for the

sample prior to weighting.

library(cobalt)

#> cobalt (Version 4.6.3, Build Date: 2026-05-29)

data("lalonde", package = "cobalt")

covs <- subset(lalonde, select = -c(treat, race, re78))

# Initialize the object with the balance statistic,

# treatment, and covariates

smd.init <- bal.init(covs,

treat = lalonde$treat,

stat = "smd.max",

estimand = "ATT")

# Compute balance with no weights

bal.compute(smd.init)

#> [1] 0.8263093

# Can also compute the statistic directly using bal.compute():

bal.compute(covs,

treat = lalonde$treat,

stat = "smd.max",

estimand = "ATT")

#> [1] 0.8263093The largest absolute standardized mean difference with no weights is

0.8263, which we can verify and investigate further using

bal.tab():

bal.tab(covs,

treat = lalonde$treat,

binary = "std",

estimand = "ATT",

thresholds = .05)

#> Balance Measures

#> Type Diff.Un M.Threshold.Un

#> age Contin. -0.3094 Not Balanced, >0.05

#> educ Contin. 0.0550 Not Balanced, >0.05

#> married Binary -0.8263 Not Balanced, >0.05

#> nodegree Binary 0.2450 Not Balanced, >0.05

#> re74 Contin. -0.7211 Not Balanced, >0.05

#> re75 Contin. -0.2903 Not Balanced, >0.05

#>

#> Balance tally for mean differences

#> count

#> Balanced, <0.05 0

#> Not Balanced, >0.05 6

#>

#> Variable with the greatest mean difference

#> Variable Diff.Un M.Threshold.Un

#> married -0.8263 Not Balanced, >0.05

#>

#> Sample sizes

#> Control Treated

#> All 429 185We can see that the largest value corresponds to the covariate

married.

Now, lets estimate weights using probit regression propensity scores in WeightIt and see whether this balance statistic decreases after applying the weights:

library("WeightIt")

w.out <- weightit(treat ~ age + educ + married + nodegree +

re74 + re75,

data = lalonde,

method = "glm",

estimand = "ATT",

link = "probit")

# Compute the balance statistic on the estimated weights

bal.compute(smd.init, get.w(w.out))

#> [1] 0.06936946After weighting, our balance statistic is 0.0694, indicating a significant improvement. Let’s try again with logistic regression:

w.out <- weightit(treat ~ age + educ + married + nodegree +

re74 + re75,

data = lalonde,

method = "glm",

estimand = "ATT",

link = "logit")

# Compute the balance statistic on the estimated weights

bal.compute(smd.init, get.w(w.out))

#> [1] 0.04791925This is better, but we can do even better with bias-reduced logistic regression (Kosmidis and Firth 2020):

w.out <- weightit(treat ~ age + educ + married + nodegree +

re74 + re75,

data = lalonde,

method = "glm",

estimand = "ATT",

link = "br.logit")

# Compute the balance statistic on the estimated weights

bal.compute(smd.init, get.w(w.out))

#> [1] 0.04392724Instead of writing each complete call one at a time, we can do a little programming to make this happen automatically:

# Initialize object to compute the largest SMD

smd.init <- bal.init(covs,

treat = lalonde$treat,

stat = "smd.max",

estimand = "ATT")

# Create vector of tuning parameters

links <- c("probit", "logit", "cloglog",

"br.probit", "br.logit", "br.cloglog")

# Apply each link to estimate weights

# Can replace sapply() with purrr::map()

weights.list <- sapply(links, function(link) {

weightit(treat ~ age + educ + married + nodegree +

re74 + re75,

data = lalonde,

method = "glm",

estimand = "ATT",

link = link) |>

get.w()

}, simplify = FALSE)

# Use each set of weights to compute balance

# Can replace sapply() with purrr:map_vec()

stats <- sapply(weights.list, bal.compute,

x = smd.init)

# See which set of weights is the best

stats

#> probit logit cloglog br.probit br.logit br.cloglog

#> 0.06936946 0.04791925 0.02726102 0.06444577 0.04392724 0.02457557

stats[which.min(stats)]

#> br.cloglog

#> 0.02457557Interestingly, bias-reduced complimentary log-log regression produced

weights with the smallest maximum absolute standardized mean difference.

We can use bal.tab() to more finely examine balance on the

chosen weights:

bal.tab(covs,

treat = lalonde$treat,

binary = "std",

weights = weights.list[["br.cloglog"]])

#> Balance Measures

#> Type Diff.Adj

#> age Contin. -0.0089

#> educ Contin. -0.0246

#> married Binary -0.0012

#> nodegree Binary 0.0145

#> re74 Contin. -0.0209

#> re75 Contin. -0.0213

#>

#> Effective sample sizes

#> Control Treated

#> Unadjusted 429. 185

#> Adjusted 240.83 185If balance is acceptable, you would move forward with these weights in estimating the treatment effect. Otherwise, you might try other values of the tuning parameters, other specifications of the model, or other weighting methods to try to achieve excellent balance.

Balance statistics

Several balance statistics can be computed by

bal.compute() and bal.init(), and the ones

available depend on whether the treatment is binary, multi-category, or

continuous. These are explained below and on the help page

?bal.compute. A complete list for a given treatment type

can be requested using available.stats(). Some balance

statistics are appended with ".mean", ".max",

or ".rms", which correspond to the mean (or L1-norm),

maximum (or L-infinity norm), and root mean square (or L2-norm) of the

absolute univariate balance statistic computed for each covariate.

In addition, balance statistics can be compute between a sample and

the same sample but weighted; this is known as “target balance” and is

important when assessing the quality of weights for continuous

treatments or for selecting a representative subset. To assess target

balance, the treatment variable should be omitted from

bal.compute() and bal.init().

smd.mean, smd.max,

smd.rms

The mean, maximum, and root mean square of the absolute standardized

mean differences computed for the covariates using

col_w_smd(). The other allowable arguments include

estimand (ATE, ATC, or ATT) to select the estimand,

focal to identify the focal treatment group when the ATT is

the estimand and the treatment has more than two categories, and

pairwise to select whether mean differences should be

computed between each pair of treatment groups or between each treatment

group and the target group identified by estimand (default

TRUE). Can be used with binary and multi-category

treatments and for target balance (where the standardization factor is

computed using the full original sample).

ks.mean, ks.max, ks.rms

The mean, maximum, or root-mean-squared Kolmogorov-Smirnov statistic,

computed using col_w_ks(). The other allowable arguments

include estimand (ATE, ATC, or ATT) to select the estimand,

focal to identify the focal treatment group when the ATT is

the estimand and the treatment has more than two categories, and

pairwise to select whether statistics should be computed

between each pair of treatment groups or between each treatment group

and the target group identified by estimand (default

TRUE). Can be used with binary and multi-category

treatments and for target balance.

ovl.mean, ovl.max,

ovl.rms

The mean, maximum, or root-mean-squared overlapping coefficient

compliment, computed using col_w_ovl(). The other allowable

arguments include estimand (ATE, ATC, or ATT) to select the

estimand, focal to identify the focal treatment group when

the ATT is the estimand and the treatment has more than two categories,

and pairwise to select whether statistics should be

computed between each pair of treatment groups or between each treatment

group and the target group identified by estimand (default

TRUE). Can be used with binary and multi-category

treatments and for target balance.

mahalanobis

The Mahalanobis distance between the treatment group means, which is

computed as \[

\sqrt{(\mathbf{\bar{x}}_1 - \mathbf{\bar{x}}_0) \Sigma^{-1}

(\mathbf{\bar{x}}_1 - \mathbf{\bar{x}}_0)}

\] where \(\mathbf{\bar{x}}_1\)

and \(\mathbf{\bar{x}}_0\) are the

vectors of covariate means in the two treatment groups, \(\Sigma^-1\) is the (generalized) inverse of

the covariance matrix of the covariates (Franklin et al.

2014). This is similar to "smd.rms" but the

covariates are standardized to remove correlations between and

de-emphasize redundant covariates. The other allowable arguments include

estimand (ATE, ATC, or ATT) to select the estimand, which

determines how the covariance matrix is calculated, and

focal to identify the focal treatment group when the ATT is

the estimand. Can only be used with binary treatments and for target

balance.

energy.dist

The total energy distance between each treatment group and the target

sample, which is a scalar measure of the similarity between two

multivariate distributions. See Huling and Mak

(2024) for

details. The other allowable arguments include estimand

(ATE, ATC, or ATT) to select the estimand, focal to

identify the focal treatment group when the ATT is the estimand and the

treatment has more than two categories, and improved to

select whether the “improved” energy distance should be used, which

emphasizes difference between treatment groups in addition to difference

between each treatment group and the target sample (default

TRUE). Can be used with binary and multi-category

treatments and for target balance.

kernel.dist

The kernel distance between treatment groups, which is a scalar measure of the similarity between two multivariate distributions. See Zhu et al. (2018) for details. Can only be used with binary treatments.

l1.med

The median L1 statistic computed across a random selection of

possible coarsening of the data. See Iacus et al.

(2011)

for details. The other allowable arguments include

l1.min.bin (default 2) and l1.max.bin default

(12) to select the minimum and maximum number of bins with which to bin

continuous variables and l1.n (default 101) to select the

number of binnings used to select the binning at the median.

covs should be supplied without splitting factors into

dummies to ensure the binning works correctly. Can be used with binary

and multi-category treatments.

r2, r2.2, r2.3

The post-weighting \(R^2\) of a

model for the treatment given the covariates. Franklin et al. (2014)

describe a similar but less generalizable metric, the “post-matching

c-statistic”. The other allowable arguments include poly to

add polynomial terms of the supplied order to the model and

int (default FALSE) to add two-way

interactions between covariates into the model. Using

"r2.2" is a shortcut to requesting squares, and using

"r2.3" is a shortcut to requesting cubes. Can be used with

binary and continuous treatments. For binary treatments, the McKelvey

and Zavoina \(R^2\) from a logistic

regression is used; for continuous treatments, the \(R^2\) from a linear regression is used.

p.mean, p.max, p.rms

The mean, maximum, or root-mean-squared absolute Pearson correlation

between the treatment and covariates, computed using

col_w_corr(). Can only be used with continuous

treatments.

s.mean, s.max, s.rms

The mean, maximum, or root-mean-squared absolute Spearman correlation

between the treatment and covariates, computed using

col_w_corr(). Can only be used with continuous

treatments.

distance.cov, distance.cor

The distance covariance or distance correlation between the scaled covariates and treatment, which is a scalar measure of the independence of two possibly multivariate distributions. See Huling et al. (2023) for details. Can only be used with continuous treatments. The distance correlation is a scaled version of the distance covariance to range from 0 to 1.

Choosing a balance statistic

Given all these options, how should one choose? There has been some

research into which yields the best results (Franklin et al.

2014; Griffin et al.

2017; Stuart et

al. 2013; Belitser et al. 2011; Parast et al.

2017), but the actual performance of each depends on the

unique features of the data and system under study. For example, in the

unlikely case that the true outcome model is linear in the covariates,

using the "smd" or "mahalanobis" statistics

will work well for binary and multi-category treatments. In more

realistic cases, though, every measure has its advantages and

disadvantages.

For binary and multi-category treatments, only

"energy.dist", "kernel.dist", and

"L1.med" reflect balance on all features of the joint

covariate distribution, whereas the others summarize across balance

statistics computed for each covariate ignoring the others. Similarly,

for continuous treatments, only "distance.cor" (or

"distance.cov") reflects balance on all features of the

joint covariate distribution. Given these advantages,

"energy.dist" and "distance.cor" are my

preferences. That said, other measures are better studied, possibly more

intuitive, and more familiar to a broad audience.

Example

In this section, I will provide an example that demonstrates how

these functions could be used to replicate the functionality of existing

packages or develop new methods for optimizing balance. We will use

these functions to replicate the functionality of WeightIt and

twang for estimating propensity score weights for a binary

treatment using generalized boosted modeling (GBM). See

?bal.compute for another example that optimizes balance to

find the number of subclasses in propensity score subclassification.

Tuning GBM for balance

GBM has many tuning parameters that can be optimized, but the key

parameter is the number of trees to use to calculate the predictions.

WeightIt and twang both implement the methods

described in McCaffrey et al. (2004) for

selecting the number of trees using a balance criterion. Here, we will

do so manually both to understand the internals of these functions and

illustrate the uses of bal.compute() and

bal.init() to select the ideal number of trees for

propensity score weighting with a binary treatment.

data("lalonde")

# Initialize balance

covs <- subset(lalonde, select = -c(treat, re78))

ks.init <- bal.init(covs,

treat = lalonde$treat,

stat = "ks.max",

estimand = "ATT")

# Fit a GBM model using *WeightIt* and `twang` defaults

fit <- gbm::gbm(treat ~ age + educ + married + race +

nodegree + re74 + re75,

data = lalonde,

distribution = "bernoulli",

n.trees = 4000, interaction.depth = 3,

shrinkage = .01, bag.fraction = 1)

trees_to_test <- 1:4000

p.mat <- predict(fit, type = "response",

n.trees = trees_to_test)

stats <- apply(p.mat, 2L, function(p) {

# Compute ATT weights

w <- ifelse(lalonde$treat == 1, 1, p / (1 - p))

bal.compute(ks.init, weights = w)

})

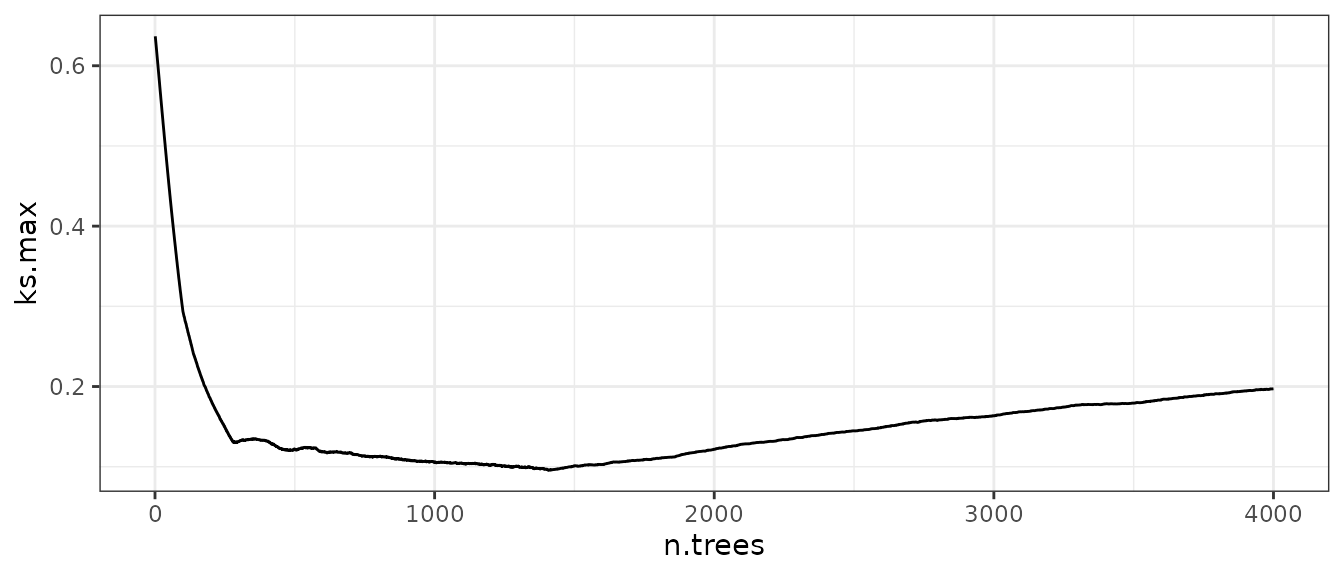

stats[which.min(stats)]

#> 1408

#> 0.09563649From these results, we see that using 1408 trees gives us the lowest maximum KS statistic of 0.0956. Out of interest, we can plot the relationship between the number of trees and our balance statistic to see what it looks like:

library("ggplot2")

ggplot() +

geom_line(aes(x = trees_to_test, y = stats)) +

theme_bw() +

labs(y = "ks.max", x = "n.trees")

Let’s compare this to the output of WeightIt:

library("WeightIt")

w.out <- weightit(treat ~ age + educ + married + race +

nodegree + re74 + re75,

data = lalonde, estimand = "ATT",

method = "gbm",

n.trees = 4000, interaction.depth = 3,

shrinkage = .01, bag.fraction = 1,

criterion = "ks.max")

# Display the best tree:

w.out$info$best.tree

#> 1

#> 1408

# ks.max from weightit()

bal.compute(ks.init, weights = get.w(w.out))

#> [1] 0.09563649We can see that weightit() also selects 1408 trees as

the optimum and the resulting maximum KS statistic computed using the

returned weights is equal to the one we computed manually. Using

twang::ps() also produces the same results.